Use our Mortgage Calculator to quickly estimate your monthly payments and plan your home purchase with confidence.

Advanced Mortgage Estimator

Complete PITI (Principal, Interest, Taxes, & Insurance) Calculation

+ Include Taxes & Insurance (Recommended)

3 Steps to Your Estimate:

- Enter the Home Price: Start with the total cost of the house.

- Adjust Your Down Payment: Aim for 20% to remove the red PMI fee from your total.

- Check the “Advanced” Toggle: We’ve pre-filled national averages for Taxes and Insurance, but you can click the toggle to customize them for your specific zip code.

Estimate Your Monthly House Payments

Buying a home is likely the most significant financial decision you will ever make. Whether you are a first-time homebuyer or looking to refinance, using a Mortgage Calculator is the essential first step in your journey. Our tool is designed to provide foolproof guidance, helping you understand exactly how much house you can afford without the technical jargon.

How to Use This Mortgage Payment Calculator

To get the most accurate results, you need to understand the key components that make up your loan. Our calculator focuses on transparency and ease of use. Simply enter your total home price, your planned down payment, and the current market interest rates.

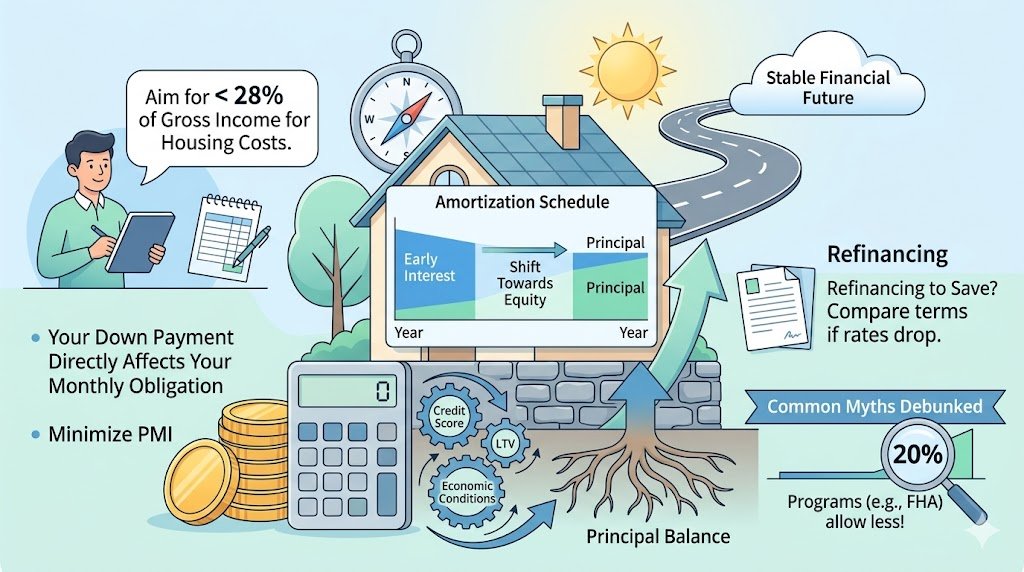

Pro Tip: Most financial experts recommend keeping your total housing costs under 28% of your gross monthly income. You can check current national averages at Bankrate to ensure your interest rate input is realistic.

Understanding Your Loan Terms

The loan term is the number of years you have to repay the debt. A 30-year fixed-rate mortgage is the most popular choice because it offers lower monthly payments, making homeownership accessible. However, a 15-year mortgage allows you to build equity faster and pay significantly less in total interest over the life of the loan.

The Importance of a Down Payment

Your down payment directly impacts your monthly obligation. While many aim for the traditional 20% to avoid Private Mortgage Insurance (PMI), many modern loan programs allow for as little as 3% or 3.5% down.

Key Factors Influencing Your Mortgage Rate

- Credit Score: Higher scores typically unlock lower interest rates.

- Loan-to-Value Ratio (LTV):</strong> The relationship between the loan amount and the home’s value.

- Economic Conditions: Rates fluctuate based on inflation and Federal Reserve policies.

How a Mortgage Amortization Schedule Works

When you first start making payments, you might notice that a large portion of your money goes toward interest rather than the principal balance. This is a process called amortization. In the early years of a 30-year mortgage, the lender front-loads the interest. As the years progress, the ratio shifts, and a larger percentage of your monthly payment begins to pay down the actual home debt. Using a mortgage calculator helps you visualize how much of your hard-earned money is building equity versus paying the bank.

When Should You Consider Refinancing?

Homeowners often revisit their mortgage terms when market conditions change. Refinancing involves replacing your current loan with a new one, typically to secure a lower interest rate or to change the loan duration. If market rates drop by 1% or more below your current rate, it may be time to use this tool to see how much you could save. Additionally, some homeowners choose a “cash-out refinance” to tap into their home’s equity for renovations or debt consolidation.

Common Mortgage Myths Debunked

Many people believe they cannot buy a home without a 20% down payment. In reality, programs like FHA loans or VA loans (available for veterans) offer much lower entry points, sometimes as low as 0% to 3.5%. Another myth is that the lowest interest rate is always the best deal; however, you must also consider closing costs and loan points. Always look at the Annual Percentage Rate (APR) for a more comprehensive view of the loan’s true cost.

By staying informed and using our foolproof estimator, you are better positioned to negotiate with lenders and secure a deal that fits your long-term financial goals. For more detailed information on government-backed loans, visit the U.S. Department of Housing and Urban Development (HUD) website.

Visit Our Home Page for More Useful Tools.